Free Credit Card Processing for Small Business: Save Big on Transaction Fees

Free Credit Card Processing for Small Business: Save Big on Transaction Fees

Natalie Luneva

January 14, 2025

Did you know small businesses can lose up to 3.5% of their revenue to merchant service fees? As a small business owner, avoiding these fees contributes to your growth and profit. Free credit card processing offers a great way to eliminate these costs.

Free credit card processing means no extra fees for credit card transactions. It uses two main ways. One adds a small fee to each purchase. The other includes the costs in the business's prices.

With no-fee processing, businesses can draw in more customers. Many people prefer not to use cash. In fact, only 20% of payments in the U.S. are in cash. More than 60% of shoppers like to pay with their preferred method. This shows how important it is to offer payment options without extra costs.

But, there are rules about adding extra fees. Most states limit surcharges to about 4%. Some states, like Colorado, let businesses pass on up to 2% of the cost to customers.

Other states, like Connecticut and Massachusetts, don't allow surcharges at all. This makes it tricky for businesses to decide on no-fee options.

Also, remember other fees that might come with no-fee processing. These can include fees for security, service, and equipment. For businesses with variable sales or thin margins, no-fee processing can help. It lets them keep prices competitive while making more money.

Choosing no-fee processing can really help your small business. It makes managing fees easier. It also helps you accept payments smoothly, even with today's complex rules.

Surcharging adds a fee to credit card transactions to cover processing costs. It's often called zero fee credit card processing. However, understand the legal and consumer aspects. Many credit card processors allow surcharging, helping businesses manage transaction costs.

In states like California and Florida, surcharging is okay but with rules. But, states like Connecticut and Massachusetts ban it. So, merchants must know the laws to stay legal.

When you use surcharging, you must tell customers about the extra fees. Visa says to tell them the fee is not more than your cost. Being open helps keep customers trusting you.

Only 21% of people don't like surcharging fees. But, seniors and baby boomers really don't like them. Knowing this can help you decide how to handle payments.

Surcharging might make some people choose cash or debit instead. This could save you money. But, it might also make some customers leave without buying.

To do surcharging right, know the local laws, tell customers about fees, and train your staff. Thinking about the good and bad of surcharging helps you choose the best payment options for your business.

Free credit card processing uses special payment processing mechanics. It changes how costs are shown to customers. When you pay with a credit card, a fee is usually added. In a zero-fee system, the terminal adds these fees to the total cost.

This makes the credit card transaction seem free to the seller. It shifts the merchant costs to the customer.

Be aware that some states have rules on surcharges. For example, surcharges can't be more than 4% of the transaction value in some places. But, in states like Connecticut and Massachusetts, surcharges are not allowed. Businesses in these states need to find other merchant solutions, such as dual pricing.

Businesses like food trucks and boutique shops often use this method. They might find that customers prefer cash or are okay with a surcharge for using credit cards. This shows how free credit card processing works in real life.

If not done right, these businesses might lose customers. Customers might choose debit cards or look for other payment options.

Here's a quick look at surcharge rules in different states:

Understanding these factors helps you see how zero-cost processing can help your business. Carefully considering your options can lead to big cost savings and happy customers.

Free credit card processing helps you save money, letting you keep more of what you earn. This way, you can make more profit, which is good for your business's health.

Choosing free processing gives you an edge over competitors. You can offer more payment options without extra costs. Studies show that accepting credit cards can double your sales, showing its value.

Quick payment processing is vital for managing cash flow. Money usually gets to your account in a few days. This is faster than other payment methods like ACH. Also, dealing with credit card disputes is easier, adding to your business's security.

Small business owners should not ignore the benefits of free credit card processing. It offers better customer service and can boost sales. This makes it a great way to increase profits and stay competitive.

Zero-fee credit card processing for small businesses comes with legal implications. In states where surcharging is okay, businesses must keep fees below the processing cost.

There are a few ways to offer zero-fee credit card processing. One method is a service fee for all customers. Another is a cash discount program, where cash payments get a discount. These methods are under the rules of credit card processing legality.

Avoid breaking surcharging rules to avoid big fines. Businesses must tell customers about surcharges before they pay.

To help understand, here's a table showing surcharging rules in different states:

These points show why it's vital to follow the law with your business. Working with providers like CardX can help. They ensure surcharges are disclosed and managed right, following state laws and rules.

When picking credit card processors for your small business, watch out for key factors. These can greatly change your costs and how well you handle payments. Look for hidden fees, understand contract terms, check transaction limits, and see how fast payments are processed.

While a processor may advertise as “free,” it’s essential to investigate the potential for hidden fees.

Before committing to a free credit card processor, carefully review the contract terms. Look out for early termination fees that may lock you into a service even if it’s not working for your business. Some processors require long-term agreements, which can be difficult to break.

If possible, choose a provider offering month-to-month contracts to retain flexibility and avoid financial penalties.

Many free credit card processors impose restrictions on how many transactions you can process or the total dollar amount you can handle each month. Exceeding these limits could result in additional charges or even service interruptions.

Be sure to understand these caps and evaluate whether they align with your business's typical transaction volume to avoid unexpected costs.

Timely access to funds helps in maintaining healthy cash flow. Different processors offer varying speeds for transferring payments to your account. Some may deposit funds within one business day, while others might take several days. Understand the processing times and any associated fees for expedited deposits to ensure the provider meets your financial needs.

A credit card processor must seamlessly integrate with your existing systems to avoid operational headaches. Check whether it works with your point-of-sale (POS) system or e-commerce platform. Compatibility ensures smooth transactions, reduces the need for costly software adjustments, and improves the overall customer experience.

Security is a non-negotiable factor when selecting a credit card processor. Ensure the provider complies with PCI DSS standards to safeguard customer data. Look for additional features like encryption and fraud detection tools to minimize risks and protect both your business and your customers from cyber threats or fraudulent transactions.

The availability and quality of customer support can significantly affect your experience with a processor. Some free processors may offer limited support options, such as email-only assistance.

Assess whether the provider offers live chat or phone support and consider the responsiveness and helpfulness of their service. Reliable support is essential, especially during peak business hours or in case of technical issues.

The processor you choose should accommodate various payment methods to meet customer preferences. Ensure it supports major credit cards like Visa, Mastercard, and American Express, as well as emerging methods such as digital wallets (e.g., Apple Pay, Google Pay). Offering multiple payment options can enhance customer satisfaction and boost sales.

As your business grows, your payment processing needs will likely evolve. Check if the processor offers premium plans or additional features, such as analytics, recurring billing, or international payment support. Choosing a processor with scalable solutions ensures that you won’t need to switch providers as your business expands.

Before committing to a processor, read user reviews and testimonials from businesses similar to yours. Look for feedback on reliability, transparency, and ease of use. Reviews can provide valuable insights into the provider’s performance and help you avoid pitfalls that others may have experienced.

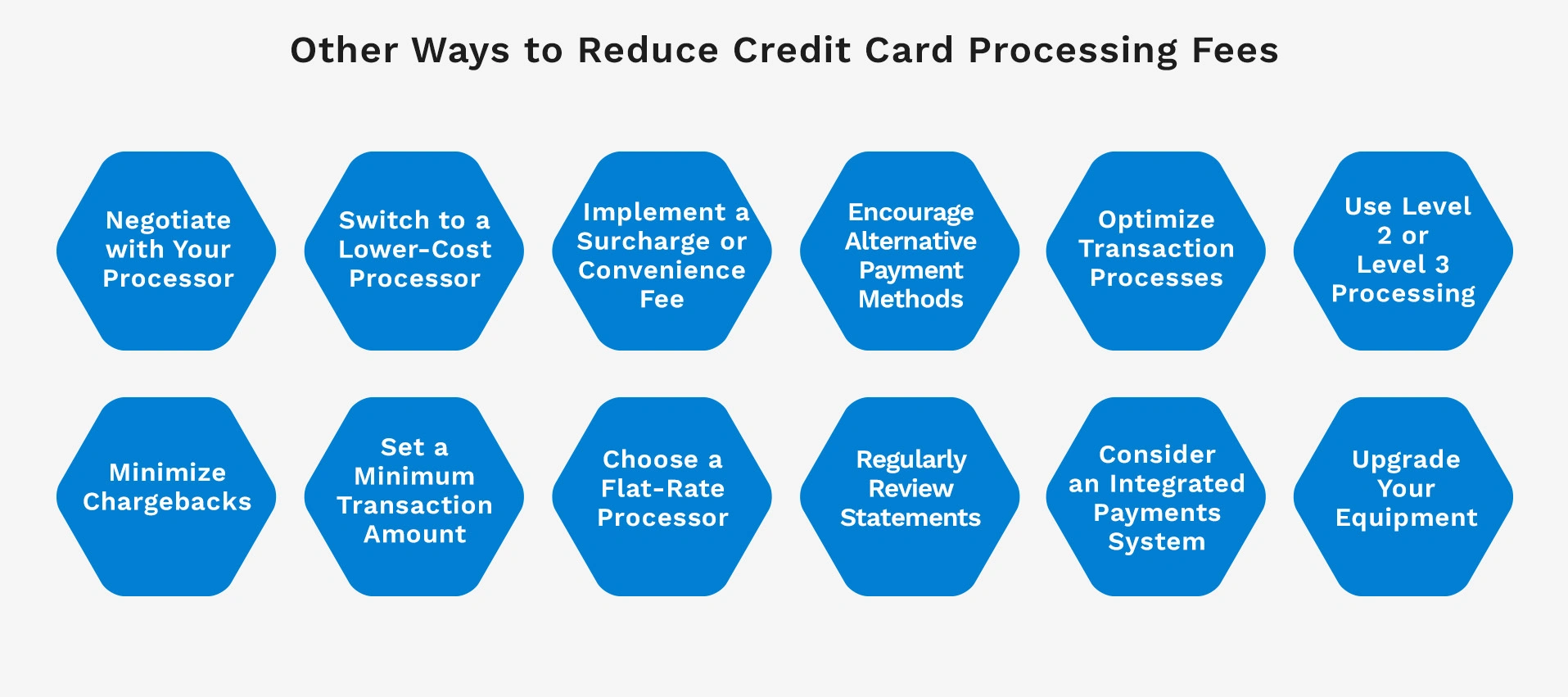

Lowering credit card fees is more than just picking a zero-fee option. Small businesses can negotiate fees and look at different payment processors. Using smart strategies and calculating your credit card processing fees can lead to big savings over time.

Credit card processors often have room for negotiation, especially if your business processes a high volume of transactions or has been a long-term customer. Reach out to your provider to discuss lower rates or discounts.

Highlight your transaction volume, timely payments, and low chargeback rates as leverage. Even small reductions in fees can add up to significant savings over time.

Take time to compare multiple credit card processors and their fee structures. Look for providers that offer transparent pricing with no hidden fees. Many newer processors offer flat-rate pricing, which could be more affordable for small businesses with predictable transaction sizes.

Ensure the provider meets your specific needs, including compatibility with your existing systems and support for your preferred payment methods.

Passing a small percentage of credit card fees to customers can help offset costs. Surcharges are generally used for credit card payments, while convenience fees are applied for specific payment methods, such as online or over-the-phone payments.

Be sure to follow local laws and credit card network rules to ensure compliance. Clearly inform customers of the fee beforehand to avoid confusion or dissatisfaction.

Encourage customers to use cash, debit cards, or bank transfers and offer small discounts or other incentives. These payment methods often have lower processing fees or no fees at all.

Clear signage at your physical location or a prompt during checkout can help customers understand their options and the benefits of using alternative payment methods.

Streamline your transaction processes to reduce unnecessary costs. For example, batch processing transactions once or twice a day can reduce the number of batch fees charged by your processor.

Additionally, prioritize using chip readers or contactless payments over manually entering card details, as keyed-in transactions tend to have higher fees due to increased fraud risk.

If your business deals with B2B or B2G transactions, take advantage of Level 2 or Level 3 data processing. These levels require additional information like customer codes or product details but often qualify for lower interchange rates.

While setup may require effort, the savings on large transactions can be substantial, making it an excellent option for businesses dealing with higher-value sales.

Chargebacks can be expensive and damage your reputation with processors. Ensure clear communication about your return and refund policies, and provide accurate product descriptions.

Offering excellent customer service can also help resolve disputes before they escalate to chargebacks, saving you both time and money.

Requiring a minimum purchase amount for credit card payments ensures that the fees you incur are proportional to the transaction value. For example, setting a $5 or $10 minimum can help reduce losses on micro-transactions where fees eat up most of the profit. Make sure to inform customers about this policy to avoid misunderstandings.

Flat-rate processors charge a single percentage for all transactions, regardless of the card type or transaction size. This model simplifies budgeting and can reduce costs if your business has consistent transaction sizes.

However, businesses with high transaction volumes or larger average ticket sizes may benefit more from interchange-plus pricing. Assess your sales patterns to choose the best option.

Processor fees can change over time, and hidden charges may creep into your monthly statements. Regularly review your statements to identify discrepancies or unexpected costs. If you spot unusual charges, contact your provider to dispute them.

Staying vigilant helps you avoid unnecessary expenses and keeps your processing costs under control.

Integrated payment systems combine credit card processing with other business functions, such as inventory management or customer relationship management (CRM). These systems can reduce overall costs, as they bundle services at discounted rates and improve operational efficiency. Choose an integrated solution that fits your industry and workflow to maximize savings.

Outdated payment terminals can lead to higher processing fees and increased vulnerability to fraud. Investing in modern equipment, such as EMV-compliant or contactless payment terminals, can help you qualify for lower rates.

Additionally, newer hardware often comes with enhanced security features, reducing the risk of fraud-related costs and improving customer trust.

Choosing the right payment processor is key for your small business's success. PayWisor helps you compare different credit card processing companies. It finds the best merchant service solutions for your needs. Knowing your business needs and using technology can boost your efficiency and profits.

When looking at payment processors, it's important to understand their fees. PayWisor helps you see the details of processing fees. This knowledge helps you make better choices.

The market has many players, like banks and fintech companies. It's important to know what they offer. PayWisor makes it easy to compare things like security and customer support.

Using PayWisor makes choosing easier and gives you insights. Whether you're looking at Square or Shopify Payments, knowing what they offer helps. The right payment processor can increase sales and improve customer satisfaction, helping your business grow.

Choosing the right payment processor is more than saving money. It's about giving your customers a great experience. With PayWisor, you can confidently find the best payment processor for your small business. Talk to our payments expert to find the best solution for you.

Zero-fee credit card processing can greatly help small businesses. It lets them save money while keeping customers happy. By understanding how it works, you can choose what's best for your business.

The world of credit card fees is complex. Zero-fee processing can be a big advantage. It helps you avoid high costs.

Remember, there are legal rules about surcharging. Knowing these rules is important as most people don't like extra fees.

Companies like Blue Yonder and Dynamic Payment Systems offer different fees. This gives you choices. It's important to look at these options carefully.

With the right information, you can choose the right credit card payment processor for your small business. This helps you keep profits up and customers happy.

Take advantage of zero-fee credit card processing. It can give you an edge over competitors. And it makes your payment processes better.