EIRF Explained: Ultimate Guide to Electronic Interchange Reimbursement Fee

Did you know that the average interchange fee for certain transactions can be as high as 3%? This shows the importance of the Electronic Interchange Reimbursement Fee, or EIRF. When credit card transactions default to EIRF, businesses often face higher costs. EIRF rates can hit 2.30% + $0.10 if transactions aren't settled in 48 hours.

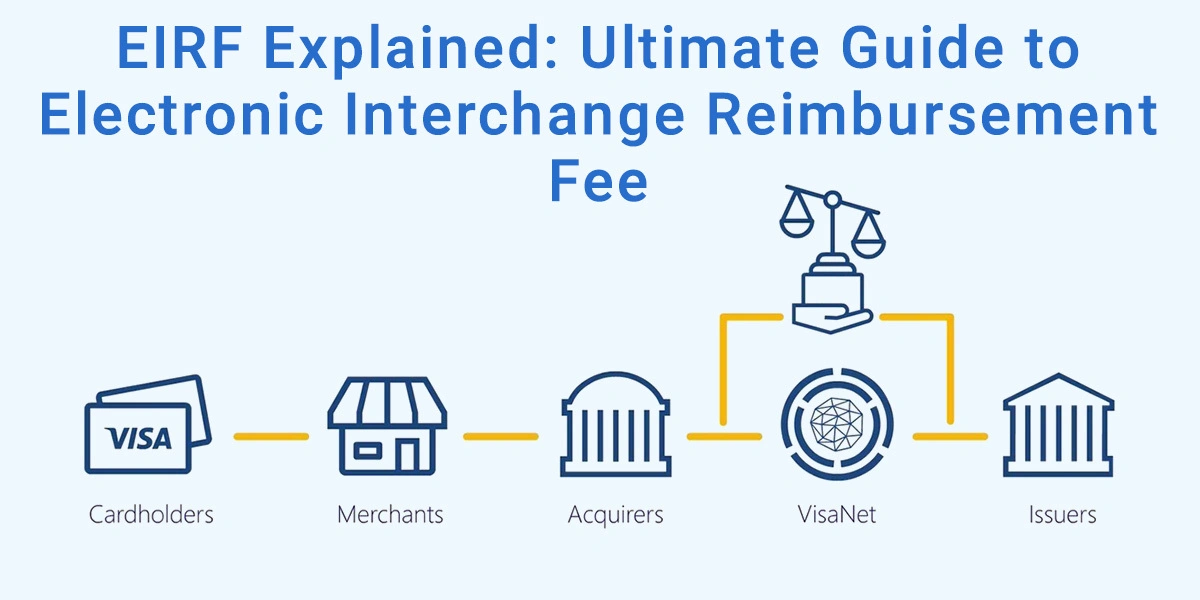

The EIRF is a part of interchange fees and only applies to Visa transactions. Many merchants don't fully understand this fee, leading to unnecessary expenses. When you learn how to avoid EIRF, you can manage your transactions better and improve your profits.

Key Takeaways

- EIRF fees can significantly increase processing costs for businesses.

- Properly settling transactions within 48 hours helps to avoid EIRF penalties.

- Address Verification Service (AVS) reeuces EIRF charges.

- Focusing solely on swipe rates may neglect important downgrade costs.

- Understanding the distinctions between EIRF and other interchange categories is vital for cost efficiency.

What is The Visa EIRF Interchange Rate?

The Visa EIRF (Electronic Interchange Reimbursement Fee) interchange rate is a mid-tier interchange rate applied to transactions that do not qualify for lower, more favorable interchange categories due to issues like delayed settlement or missing data.

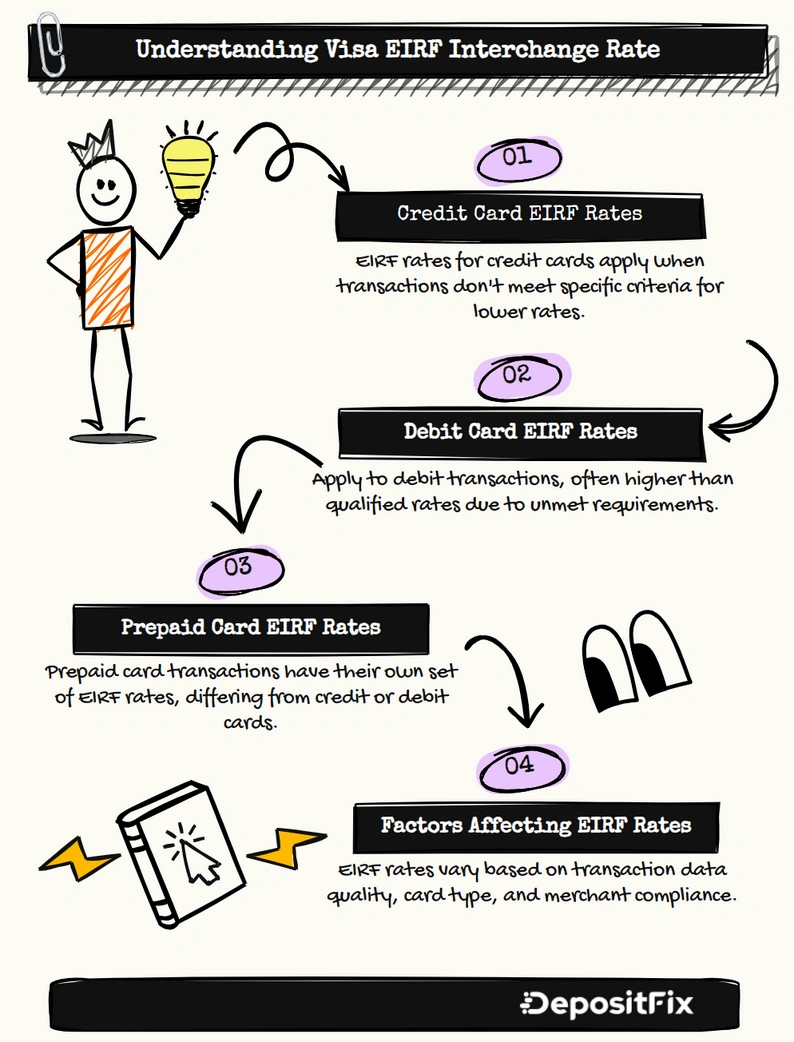

Credit Card EIRF Rates

Credit card processing fees with Visa EIRF range 2.30% plus $0.10 per transaction. These rates mainly apply to online sales. This is important when selling online.

Debit Card EIRF Rates

Debit card rates with Visa EIRF vary. Standard transactions cost 1.75% plus $0.20. But, regulated debit transactions are much cheaper, at 0.05% plus $0.21. The type of retail environment can also change these rates.

Prepaid Card EIRF Rates

Prepaid card rates with Visa EIRF are 1.80% plus $0.20 per transaction. This makes prepaid card rates easy to predict for everyone. Remember, these rates can change as Visa updates its fees.

What Causes Downgrades?

Interchange downgrades happen when a transaction doesn't meet certain criteria. This makes it more expensive for businesses. It's important for companies to know why these downgrades occur to cut down on fees. Common reasons include:

- Failing to settle transactions within the required 48-hour window.

- Not using the Address Verification System (AVS) for card-not-present transactions.

- Mismatches between authorization and settlement amounts.

- Not entering tax and tips separately from the transaction total.

- Having outdated terminal software.

Authorization issues can also cause downgrades. This happens when a merchant doesn't get a valid electronic authorization during the transaction. To reduce downgrades, businesses should follow best practices. For instance:

- Make sure to use AVS for all relevant transactions.

- Automate daily batch settlements to avoid missing deadlines.

- Keep your payment processing equipment up to date.

When businesses address these areas, they can improve their transaction flow. This can help lower processing fees related to interchange downgrades. Following transaction criteria will get you lower interchange rates and help you avoid extra costs.

Consumer Credit EIRF Interchange

The Consumer Credit EIRF (Electronic Interchange Reimbursement Fee) interchange is a Visa interchange category applied to certain consumer credit card transactions that fail to meet the criteria for lower interchange rates.

Electronic Interchange Reimbursement Fee

For many, the rate is 2.30% plus $0.10 per transaction. This rate is for card-present or key-entered transactions.

These transactions need electronic authorization and settle in two days. Any changes can raise your costs.

Signature Card Electronic

Signature Card Electronic transactions have a special spot. They include rewards cards at Travel and Entertainment (T&E) merchants. They have the same rate as the Electronic Interchange Reimbursement Fee.

This category is not a downgrade for these businesses. Knowing about Signature Card Electronic can improve your transaction efficiency and cost control.

Category

Rate

Transaction Type

Electronic Interchange Reimbursement Fee

2.30% + $0.10

Card-present, Key-entered

Signature Card Electronic

Same as EIRF

T&E Merchant Transactions

Consumer Debit EIRF Interchange

The Consumer Debit EIRF (Electronic Interchange Reimbursement Fee) interchange is a Visa interchange category applied to certain consumer debit card transactions that do not meet the criteria for lower interchange rates.

EIRF Debit

The EIRF Debit rate is 1.75% plus a $0.20 transaction fee. This rate applies to transactions that meet certain criteria. These include timely settlement and a valid electronic authorization.

EIRF Debit Reg

The EIRF Debit Reg category deals with regulated debit cards, mainly from big banks. These cards have a capped interchange rate: 0.05% plus a $0.22 transaction fee. Businesses using these cards often see lower interchange fees. Knowing these details helps in making better payment processing choices.

Category

Rate

Transaction Fee

Criteria

EIRF Debit

1.75%

$0.20

Timely settlement, valid electronic authorization

EIRF Debit Reg

0.05%

$0.22

Regulated debit cards from large banks

When businesses understand these consumer debit EIRF categories, they can better manage transaction costs. This leads to more informed payment processing decisions.

Consumer Prepaid EIRF Interchange

The Consumer Prepaid EIRF (Electronic Interchange Reimbursement Fee) interchange is a Visa interchange category applied to certain prepaid card transactions that fail to meet the criteria for lower interchange rates.

The standard interchange rate for EIRF Prepaid transactions is 1.80%. There's also an extra fee of $0.20 per transaction. These rates apply when transactions meet certain criteria and settle on time.

The deadline for interchange reimbursement fees is October 19, 2024. This means businesses need to check their compliance plans. Different fees apply to various prepaid card types. Here are some important fee details for consumer prepaid cards:

Transaction Type

Fee Structure

Exempt Visa Consumer Prepaid Card (Supermarket)

1.15% + $0.15 (Cap: $0.35)

Regulated Visa Consumer Prepaid Card (Supermarket)

0.05% + $0.21

Exempt Visa Consumer Prepaid Card (Utility Recurring Bill Payment)

$0.45

Regulated Visa Consumer Prepaid Card (Utility Recurring Bill Payment)

0.05% + $0.21

Knowing about the consumer prepaid EIRF helps manage transactions and cut down on fees. Paying close attention to electronic authorization and settlement times can lower your costs.

Target Interchange Categories that Downgrade to EIRF

Many target interchange categories can downgrade to EIRF if certain transaction criteria are not met. Businesses often face downgrades to EIRF, showing challenges in processing transactions. The Electronic Interchange Reimbursement Fee is a lower-tier fee for transactions that don't meet the requirements.

Is EIRF the lowest possible downgrade?

EIRF is a downgrade, but it's not the cheapest option. Transactions not meeting EIRF criteria can end up in more expensive categories, like Standard interchange.

For Visa transactions, EIRF's credit rate for Signature cards is 2.40% + $0.10. Other Visa credit cards have a rate of 2.30% + $0.10. Both are lower than the Standard credit rate for Signature cards, which is 2.95% + $0.10.

Missing details like dates, amounts, and merchant names can be costly. Expired authorizations also add to the financial burden. Using Address Verification Systems for e-commerce can help reduce fraud and improve fee accuracy.

In summary, while EIRF is a downgrade, failing to meet its criteria can lead to higher costs in the Standard category. This highlights the importance of businesses maintaining accurate and strict transaction processing standards.

EIRF on Credit Card Statements

Your EIRF credit card statement might show the Electronic Interchange Reimbursement Fee. This fee is for certain Visa transactions that don't meet specific conditions.

Transaction fees can go up if batch settlements aren't done in two days. Standard settlements take three days. If a transaction amount is off from what was authorized, it might lead to EIRF downgrades. This is especially true for certain merchant types that don't allow such changes.

The way merchant fees are shown on your statement can be confusing. Many transactions might be labeled as one EIRF charge. This makes it hard to see which transactions caused the fee. Sometimes, missing details like CVV codes or address verification can also lead to extra EIRF charges.

Businesses dealing with EIRF rates might face fees up to 2.30%. But, the actual interchange rates could be as low as 1.54%. This means there could be an extra cost of 76 basis points because of missing transaction data.

For example, if you process $8,162 in transactions, the 76 basis points could mean an extra $62.03 charge. This is because of missing information in the transactions. Such fees can be a big financial burden, especially if transactions aren't batched on time or if the wrong amounts are used.

Understanding your EIRF credit card statement can help you manage your credit card processing costs better. It gives you valuable insights into your financial situation.

Downgrade Reports

For businesses, analyzing downgrade reports will help you control credit card fees. These reports from credit card processors show why some transactions cost more. When you understand these reports, you can find out why fees went up.

Downgrades often happen because of the type of card used or missed criteria. For example, if a transaction doesn't settle in 24 hours, it might cost more. Regularly checking these reports helps spot patterns, like issues with card-not-present transactions.

Looking at these reports can reveal why costs are higher. It might be because of wrong addresses or card strip problems. Fixing these issues can stop downgrades and lower fees. This way, businesses can handle transactions better and save money.

Also, tracking these reports over time helps compare different pricing models. Knowing why downgrades happen lets you manage your processing better. This can improve your profits and control costs.

Get Transparent Credit Card Processing Fees with PayWisor

PayWisor offers tools to help you see through credit card processing clearly. You can track and analyze fees, like the Electronic Interchange Reimbursement Fee (EIRF).

The EIRF is the first fee when Visa transactions are downgraded.

For example, Visa Signature cards have a higher EIRF rate than other Visa cards. This difference can affect your expenses a lot if not managed well.

- EIRF Interchange Rate for Consumer Credit Cards: 2.30% + $0.10

- EIRF Debit rate: 1.75% + $0.20

- Consumer Prepaid Card EIRF: 1.80% + $0.20

PayWisor lets you track important details for qualifying transactions. You need to make sure they are card-present or key-entered. Also, they must be settled within two days. PayWisor's tools help you avoid costly downgrades.

Choosing transparent credit card processing changes how you make financial decisions. With PayWisor, your business can make payments smoother. This improves your credit card processing experience and helps control costs.

Conclusion

Any business that deals with credit and debit cards must be aware of EIRF. The fee for late transactions has gone up from 1.54% + $0.10 to 2.30% + $0.10. This change shows how important it is to settle transactions on time.

Businesses need to understand what causes EIRF downgrades. Making sure your AVS details are correct and handling authorizations well can save money. Also, having a plan for now and the future helps control costs better.

Being proactive in payment processing can save money. When you set goals and talk clearly with your payment teams, you can handle changes from Visa better. So, paying close attention to your card transaction processes is vital for keeping your business running smoothly.

FAQs

What is the primary purpose of EIRF?

The primary purpose of EIRF is to categorize transactions that do not meet the criteria for lower interchange rates. It serves as a default or penalty category, ensuring that transactions still process even if they don't qualify for a more favorable rate.

How can businesses avoid EIRF downgrades?

Businesses can avoid EIRF downgrades when they ensure prompt transaction settlements, using the Address Verification System (AVS), and making sure the authorization amount matches the settlement amount. Regularly reviewing downgrade reports can also help identify and rectify issues.

Does EIRF affect international transactions?

Yes, EIRF can apply to international transactions if they do not meet the necessary criteria for lower interchange categories. This includes meeting settlement timelines and authorization requirements.

Can EIRF rates change over time?

Yes, Visa periodically reviews and adjusts interchange rates, including EIRF. Changes may depend on various factors, such as regulatory changes or updates in Visa’s pricing structure.

Does EIRF impact small businesses differently than large enterprises?

The impact of EIRF is proportional to transaction volume and average transaction value. While the rates remain the same, small businesses may feel the cost more acutely due to tighter profit margins.